Mar 10, 2026

Auto Loan Delinquencies Just Hit an All-Time Record. Here's What Separates the Lenders Who'll Come Through.

Subprime auto delinquencies just hit an all-time record. Here's what it means for your servicing operation.

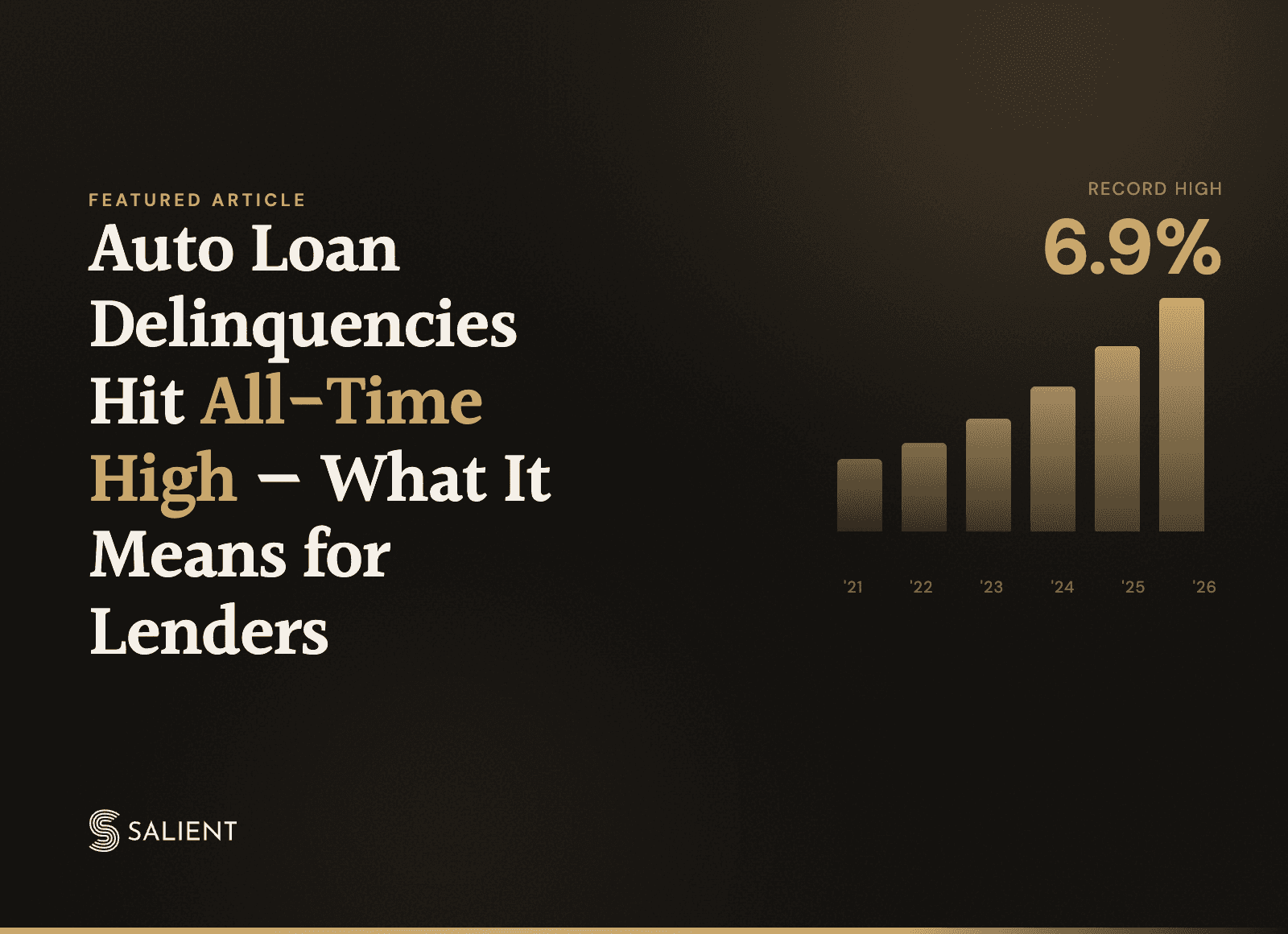

Three days ago, Axios reported that Americans are behind on car payments at a record level. The data behind that story: Fitch Ratings' January 2026 figures show the 60-day-plus delinquency rate on subprime auto loans at 6.9% — the highest rate Fitch has ever recorded since it began tracking in 1993.

Not a near-record. An all-time record.

But here's what the headline doesn't tell you: the lenders struggling most right now aren't struggling because their portfolios are bad. They're struggling because their servicing operations were built for normal cycles, not stress ones.

The delinquency surge is a stress test. And it's exposing which collections and servicing stacks were actually built to scale.

This article breaks down what's driving the surge, how subprime and prime portfolios are diverging, and what the rising delinquency rates mean for collections operations and compliance teams trying to respond at scale.

Current Auto Loan Delinquency Rates and Historical Context

According to Fitch Ratings' January 2026 data, 6.9% of subprime auto loans packaged into ABS were 60 or more days past due — the highest rate ever recorded. That figure is up from 6.65% reported in October 2025, meaning the trend is still moving in the wrong direction heading into Q1 close.

So what exactly counts as a delinquency? It's simply a missed payment, and lenders track them in 30-day increments:

30 days past due: One missed payment cycle. Lenders typically begin outreach here.

60 days past due: Two consecutive missed payments. This is the threshold most industry reports cite.

90+ days past due: Often called "serious delinquency," and it frequently leads to default or repossession.

The last time rates approached this level was during the early 1990s recession. Even during the 2008 financial crisis, subprime auto delinquencies didn't climb this high. What makes the current environment different is that there's no single economic shock driving it — instead, several structural pressures have converged at once.

Why Auto Loan Delinquencies Are Surging

The surge in delinquencies isn't happening because borrowers suddenly stopped caring about their car payments. It's happening because economic conditions shifted faster than household budgets could absorb.

Vehicle Prices Have Outpaced Income Growth

New vehicle transaction prices now average above $48,000 — up more than 30% from pre-pandemic levels. Used car prices, while down from their 2022 peaks, remain elevated too.

Higher prices translate directly into larger loan amounts and longer terms, often stretching to 72 or 84 months. Borrowers start out stretched thin, with little cushion when something goes wrong.

Higher Interest Rates Increased Monthly Payments

The Federal Reserve's rate increases between 2022 and 2024 pushed auto loan APRs higher across the board. Average rates on new car loans climbed above 7%, while subprime borrowers often pay 12% or more.

To put that in perspective: on a $35,000 loan, the difference between a 5% and 10% APR adds roughly $100 to the monthly payment. Multiply that across millions of borrowers, and the impact becomes clear.

Pandemic-Era Loan Modifications Are Expiring

During COVID-19, many lenders offered deferrals, forbearance, and payment extensions. Those programs helped borrowers stay current during acute disruption.

Now, those modifications are expiring. Deferred payments are coming due, and borrowers who were already stretched are facing catch-up obligations they can't absorb.

Inflation Has Squeezed Household Budgets

Rising costs for housing, food, fuel, and insurance have consumed a larger share of household income. When essentials take priority, car payments often slip.

Lower-income borrowers feel this most acutely. They have less margin to absorb cost increases without missing payments.

Subprime Auto Loan Delinquencies Hit Record Levels

The headline numbers are driven almost entirely by subprime borrowers — typically defined as those with credit scores below 620. Meanwhile, prime borrower performance has remained relatively stable, creating what analysts call a "K-shaped" divergence.

Subprime Borrowers Face the Steepest Delinquency Rates

Among subprime auto borrowers, 6.9% were 60 or more days past due as of January 2026 — the highest rate Fitch has ever recorded. TransUnion's 2026 credit forecast, released in December, projects this marks the fifth straight year of rising delinquencies across the overall auto loan market, with no meaningful reversal expected through year-end.

These aren't marginal increases. They represent a structural shift in how subprime portfolios are performing — and for lenders with meaningful subprime exposure, the operational pressure is arriving right now, at the close of Q1.

Prime Borrowers Remain Relatively Stable

Delinquency rates among prime borrowers have barely moved. This divergence suggests the stress is concentrated among borrowers who were already financially vulnerable, rather than reflecting broad-based consumer distress.

For lenders with mixed portfolios, the operational burden is uneven. Subprime segments require disproportionate collections resources while prime segments perform as expected.

Auto Loan Default Rates and Repossession Trends

Delinquency and default are related but distinct concepts. Understanding the difference matters for both borrowers and the lenders managing these accounts.

Delinquency: A missed payment. The account is past due but not yet written off.

Default: Prolonged non-payment, typically 90+ days. The lender considers the loan unlikely to be repaid in full.

Repossession: The lender takes possession of the vehicle, usually following default, and sells it to recover losses.

Repossession activity has increased alongside delinquencies. Industry estimates suggest 1.73 million vehicles were repossessed in 2024 — the highest number since 2009. That said, many lenders prefer to pursue payment arrangements before repossessing, given the costs and operational complexity involved.

Is an Auto Loan Bubble Forming, or Are Credit Risks Contained?

Rising delinquencies naturally raise questions about systemic risk. Is this the beginning of an auto loan bubble?

The short answer: stress is elevated, but risks appear concentrated rather than systemic. Subprime portfolios are under pressure, while prime portfolios remain stable. Unlike the 2008 mortgage crisis, auto loans represent a smaller share of household debt, and securitization structures have generally held up.

That said, lenders with significant subprime exposure face real challenges. Charge-offs are rising, loss reserves are increasing, and collections teams are stretched. The risk isn't a market-wide collapse — it's operational strain on the lenders most exposed to subprime borrowers.

What Rising Delinquency Rates Mean for Collections Operations

The headline is about borrowers. The operational reality lands on collections and servicing teams — and that's where the stress test gets real.

Collections Volume Is Outpacing Staff Capacity

More delinquent accounts mean more required outreach — calls, texts, emails, and follow-ups. Most collections teams were sized for pre-pandemic delinquency rates. They're now handling significantly more volume without proportional headcount increases.

Hiring and training collectors takes months. Delinquency surges happen in weeks. That gap is where operational strain turns into missed cures and higher charge-offs.

Right-Party Contact Rates Are Declining

Right-party contact (RPC) refers to actually reaching the borrower — not a voicemail or wrong number. As volume increases, RPC rates typically decline. Agents have less time per account, and borrowers screen unfamiliar calls.

Lower RPC rates mean fewer payment arrangements, longer delinquency cycles, and higher eventual charge-offs. The problem compounds itself.

Charge-Offs and Loss Reserves Are Climbing

A charge-off occurs when a lender writes off a loan as a loss, typically after 120-180 days of non-payment. As delinquencies age, charge-off rates follow.

Lenders are increasing loss reserves to account for expected losses, which affects profitability and capital ratios. For some institutions, this creates pressure to reduce originations or tighten underwriting.

How Lenders Can Manage Delinquent Accounts at Scale

The challenge isn't identifying the problem. It's responding at scale without proportionally increasing costs or compliance risk. The lenders handling this cycle best have stopped trying to solve a volume problem with headcount — and started rethinking the operational model entirely.

Deploy AI Agents for Inbound and Outbound Collections

AI voice agents can handle borrower conversations across phone, SMS, and email — covering payment reminders, hardship discussions, and promise-to-pay arrangements. Unlike traditional IVRs, modern AI agents navigate complex conversations and take action directly in loan servicing systems.

Lenders currently using AI-first servicing have cut average handle times by 60% and maintained compliance across 100% of interactions — without adding agent headcount. Every interaction is logged at the transcript level, generating the audit trail regulators expect.

Automate Early-Stage Collections Outreach

Reaching borrowers earlier improves cure rates significantly. A borrower at 15 days past due is far more likely to cure than one at 60 days. Automation enables consistent, proactive contact before accounts age into serious delinquency.

If early outreach cures even 5-10% more accounts before they reach 60 days, the downstream impact on charge-offs is substantial — often the difference between a manageable cycle and a reserve crisis.

Improve Right-Party Contact and Promise-to-Pay Rates

AI agents with borrower-level memory can personalize outreach — referencing prior conversations, acknowledging hardship notes, and avoiding repeated questions. When a borrower feels recognized rather than processed, they're more likely to engage and commit to a payment arrangement.

Standardize Scripting and Disclosures Across Channels

Consistency matters for both compliance and borrower experience. AI agents deliver the same disclosures, the same tone, and the same options every time — regardless of channel or time of day. This eliminates the variability that comes with human agents handling high volumes under time pressure.

Compliance Considerations for Scaling Auto Loan Collections

Scaling collections introduces compliance risk. Higher volume means more opportunities for errors — and more scrutiny from regulators. The CFPB made its position clear in August 2024: "There are no exceptions to the federal consumer financial protection laws for new technologies." That applies to every AI tool touching borrower interactions.

FDCPA and UDAAP Requirements in High-Volume Environments

Two frameworks govern most collections activity:

FDCPA (Fair Debt Collection Practices Act): Prohibits harassment, false statements, and unfair practices in debt collection. Requires specific disclosures and limits on contact frequency.

UDAAP (Unfair, Deceptive, or Abusive Acts or Practices): A broader standard enforced by the CFPB that applies to first-party collectors and servicers, not just third-party agencies.

Scaling collections without scaling compliance oversight creates real exposure. Every additional call is an additional opportunity for a violation. The lenders coming through this cycle cleanly have compliance built into their servicing infrastructure — not bolted on after the fact.

Documentation and Audit Readiness for Examiner Scrutiny

Regulators expect lenders to document what was said, what was done, and why — for every borrower interaction, not just escalated cases.

AI agents that log interactions at the transcript level, with timestamps and action records, provide the documentation examiners expect. Manual processes rarely achieve this level of consistency at scale.

Contact Frequency Caps and Time-of-Day Restrictions

Regulations limit when and how often lenders can contact borrowers. TCPA restricts calls before 8 AM and after 9 PM local time. The CFPB's Regulation F limits call attempts to seven per week per debt.

Automation configured within these guardrails ensures compliance at scale. Manual tracking of contact frequency across thousands of accounts is error-prone — and the violations that result are preventable.

How AI Collections Agents Help Lenders Navigate Delinquency Surges

Rising delinquencies create a capacity problem that traditional staffing models can't solve economically. Hiring and training collectors takes months; delinquency surges happen in weeks.

AI agents purpose-built for compliant lending offer a different path. They extend coverage to 100% of delinquent accounts, operate across voice, SMS, and email, and maintain compliance guardrails on every interaction. They integrate with existing loan servicing systems, write outcomes back in real time, and generate the documentation regulators expect.

The lenders who've moved fastest here aren't the largest ones. They're the ones who recognized that the servicing model built for normal cycles would fail under stress — and rebuilt before the stress arrived.

For lenders facing the highest delinquency rates in three decades, the question isn't whether to modernize servicing operations. It's whether to do it before Q2, or after it.

Q1 ends March 31. If your collections team is heading into the next cycle with the same stack it had last year, let's talk about what's possible →

FAQs About Auto Loan Delinquencies

How is auto loan delinquency different from default? A delinquency occurs when a borrower misses a scheduled payment. A default typically occurs after prolonged non-payment — often 90 or more days — when the lender considers the loan unlikely to be repaid in full.

What happens when a borrower defaults on a car loan? The lender typically repossesses the vehicle, sells it at auction, and may pursue the borrower for any remaining deficiency balance — the difference between the sale price and the outstanding loan amount.

How long can a borrower be delinquent before repossession begins? Timelines vary by lender and state law. Most lenders initiate repossession proceedings after 60-90 days of missed payments, though some begin earlier depending on portfolio strategy and state requirements.

Are car repossessions increasing alongside auto loan delinquencies? Yes. Repossession activity has risen as delinquencies climb, with an estimated 1.73 million vehicles repossessed in 2024. However, many lenders prefer to pursue payment arrangements before repossessing, given the costs involved.

How do lenders report delinquent auto loans to credit bureaus? Lenders typically report to credit bureaus once a payment is 30 days past due, with updates at each subsequent 30-day interval. A 60-day delinquency appears as a more serious negative mark than a 30-day delinquency.